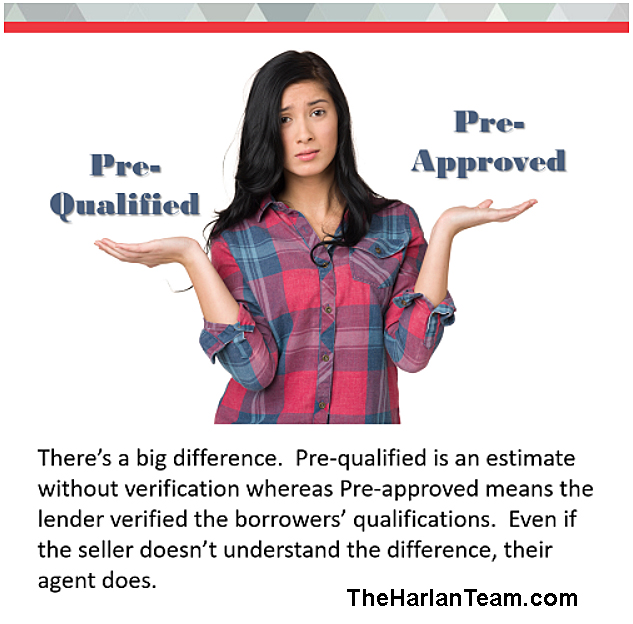

Page 5 of 12

Homeowner DIY Mistakes

Do-it-yourself home improvement can be a great way to add value to your home without having to pay builders or plumbers to do the work. But even the simplest of DIY jobs can quickly turn into an expensive mess when tackled incorrectly.

Avoid these common, and ultimately expensive, DIY mistakes:

1. UNREALISTIC GOALS: Home improvement can be an addictive hobby and many enthusiasts fall into the trap of running before they can walk. Start with small projects and work your way up to avoid compounding any problems.

2. POOR SAFETY: Falling off a ladder, inhaling fumes and slicing open fingers are just a few of the common DIY-related injuries. These accidents not only cause physical pain, but they can also affect your ability to work, and therefore, your income. You are advised to read the instruction manuals that come with any tools you purchase. While painting, be sure to open any windows to help keep the air free of dangerous fumes.

3. NOT ASKING PERMISSION: Many homeowners tackle major home improvements without first getting permission from the local authorities. Fines for unapproved work can be hefty. Many insurance companies also require proof that an improvement project followed official government guidelines.

4. CUTTING CORNERS: Tight budgets are a reality for many homeowners. It may be tempting to choose tools and materials that are more wallet-friendly, but in the long run, the investment in higher grade materials will be worth it.

5. WRONG MEASUREMENTS: Planning is a vital part of any project. All veteran home improvers follow the golden rule; measure twice, cut once.

Auto Pay Your Mortgage Payment

In the time that it takes to write one check, you can set it up with your bank and never have to do it again. You won’t have to write checks, envelopes or purchase stamps anymore. You’ll save time, money and benefit in other ways too.

In the time that it takes to write one check, you can set it up with your bank and never have to do it again. You won’t have to write checks, envelopes or purchase stamps anymore. You’ll save time, money and benefit in other ways too.

- Never be late … avoid late fees and protect your credit

- Schedule additional principal contributions monthly to save interest, build equity and shorten the mortgage term.

An extra $200 a month applied to the principal on a $200,000 mortgage at 4.5% for 30 years will result in shortening the loan by 8.5 years. If the loan was paid to term, it would save $52,977 in interest. Use the Equity Accelerator to see how much you can save. - It’s convenient … by doing it online with your bank, you’ll have a centralized history of the payments.

- Protect your credit … your payment history is the single biggest component of your credit score and accounts for over 1/3 of your credit score.

Establishing the practice of auto bill pay could run the risk of overdrawing an account and incurring overdraft charges. Monitor your bank account to be sure that you have enough cash to cover your automatic payments.

Schedule the Auto Pay to allow for processing and the time it takes to reach the lender so that you don’t incur late fees.

And even though, you set up the Auto Pay, it is still your responsibility to monitor your bank account to see that they are executing it properly. If you are making additional principal contributions, you must see that the extra amount was indeed applied to principal reduction and not somewhere else like in the escrow account.

Some banks offer email or text reminders to let you know when checks are about to be written or if your balance is low.

A To-Do List for Better Homeowners

Checklists work because they contain the important things that need to be done. They provide a reminder about things we know and realize but may have slipped our minds as well as inform us about things we didn’t consider. Periodic attention to these areas can protect the investment in your home.

Checklists work because they contain the important things that need to be done. They provide a reminder about things we know and realize but may have slipped our minds as well as inform us about things we didn’t consider. Periodic attention to these areas can protect the investment in your home.

- Change HVAC filters regularly. Consider purchasing a supply of the correct sizes needed online and they’ll even remind you when it’s time to order them again.

- Change batteries in smoke and carbon monoxide detectors annually.

- Create and regularly update a Home Inventory to keep track of personal belongings in case of burglary or casualty loss.

- Keep track of capital improvements, with a Homeowners Tax Guide, made to your home throughout the year that increases your basis and lowers gain.

- Order free credit reports from all three bureaus once a year at www.AnnualCreditReport.com.

- Challenge your property tax assessment when you receive that year’s assessment when you feel that the value is too high. We can supply the comparable sales and you can handle the rest.

- Establish a family emergency plan identifying the best escape routes and where family members should meet after leaving the home.

- If you have a mortgage, verify the unpaid balance and if additional principal payments were applied properly. Use a Equity Accelerator to estimate how long it will take to retire your mortgage.

- Keep trees pruned and shrubs trimmed away from house to enhance visual appeal, increase security and prevent damage.

- Have heating and cooling professionally serviced annually.

- Check toilets periodically to see if they’re leaking water and repair if necessary.

- Clean gutters twice a year to control rainwater away from your home to protect roof, siding and foundation.

- To identify indications of foundation issues, periodically, check around perimeter of home for cracks in walls or concrete. Do doors and windows open properly?

- Peeling or chipping paint can lead to wood and interior damage. Small areas can be touched-up but multiple areas may indicate that the whole exterior needs painting.

- If there is a chimney and fires are burned in the fireplace, it will need to be inspected and possibly cleaned.

- If the home has a sprinkler system, manually turn the sprinklers on, one station at a time to determine if they are working and aimed properly. Evaluate if the timers are set properly. Look for pooling water that could indicate a leak underground.

- Have your home inspected for termites.

Instead of remembering when you need to do these different things, use your calendar to create a system. As an example, make a new appointment with “change the HVAC filters” in the subject line. Select the recurring event button and decide the pattern. For instance, set this one for monthly, every two months with no end date. You can schedule a time or just an all-day event will show at the top of your calendar that day.

By scheduling as many of these items as you can, you won’t forget that they need to be done. If you don’t delete them from the calendar, you’ll continue to be “nagged” until you finally do them.

If you have questions or need a recommendation of a service provider, give us a call at (206) 979-9632. We deal with issues like this regularly and have experience with workers who are reputable and reasonable.