Page 7 of 12

Eliminate FHA Mortgage Insurance

Mortgage insurance premiums can add almost $200 to the payment on a $265,000 FHA mortgage. The decision to get a FHA loan may have been the lower down payment requirement or the lower credit score levels, but now that you have the loan, is it possible to eliminate it?

Mortgage Insurance Premiums protect lenders in case of a borrower’s default and is required on FHA loans. The Up-Front MIP is currently 1.75% of the base loan amount and paid at the time of closing. Annual MIP for loans with greater than 95% loan-to-value is .85% per year.

For loans with FHA case numbers assigned before June 3, 2013, when the loan is paid down to 78% of the original loan amount, the MIP can be cancelled. The borrower may need to contact the current servicer.

However, for loans greater than 90% with FHA case numbers assigned on or after that date, the MIP is required for the term of the loan.

Most homeowners with FHA mortgages are not eligible to cancel the MIP because they either originated their loan after June 3, 2013, put less than 10% down payment and/or got a 30-year loan. If they have at least 20% equity in the home, they can refinance the home with an 80% conventional loan which in most cases, does not require mortgage insurance.

With normal amortization on a 30-year loan, it takes approximately 11-years to reduce the original loan to the 78-80% requirement based on normal amortization. There is another dynamic involved which is the appreciation on the home. As the home goes up in value and the unpaid balance goes down, the equity increases.

If the homeowners believe that they have enough equity that would eliminate the need for mortgage insurance, they can investigate refinancing with a conventional loan. Borrowers refinancing will incur expenses in starting a new mortgage and the interest rate may be higher than the existing rate. Analysis will determine how long it will take to recapture the cost of refinancing.

Call me at (206) 979-9632 for a recommendation of a trusted mortgage professional.

More Millennials Plan To Be Homeowners

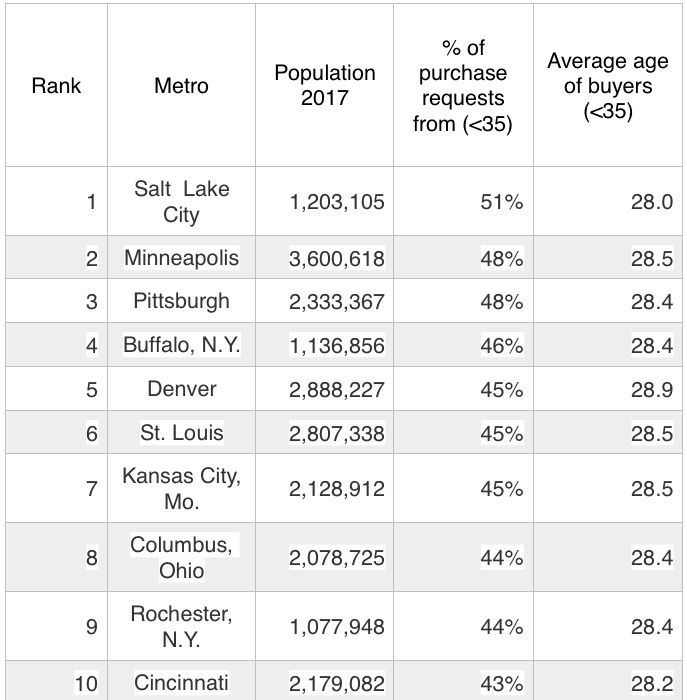

A November 2018 study conducted by the online lending firm LendingTree reported that more millennials as defined by those born between 1982 and 2002 are thinking about becoming homeowners. In fact a full 21% of those surveyed between the ages of 18 to 34 said they plan to purchase a home in the next 12 months. That is up from 14% just a year ago.

A November 2018 study conducted by the online lending firm LendingTree reported that more millennials as defined by those born between 1982 and 2002 are thinking about becoming homeowners. In fact a full 21% of those surveyed between the ages of 18 to 34 said they plan to purchase a home in the next 12 months. That is up from 14% just a year ago.

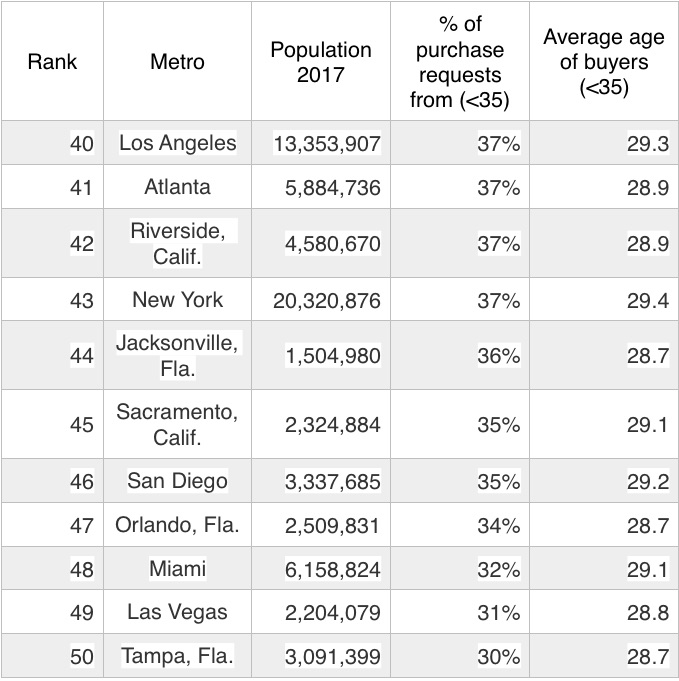

LendingTree scoured their database on new mortgage purchase requests to learn where millennials planned to buy.

The Top 10 Cities

The Bottom 10 Cities

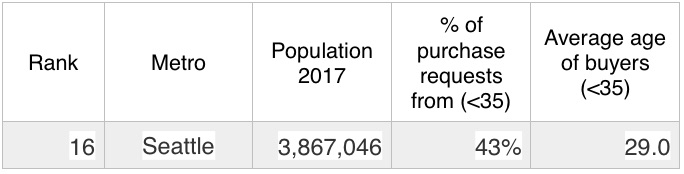

So where did Seattle land on the list?

Where Are Interest Rates Headed in 2019?

The interest rate you pay on your home mortgage has a direct impact on your monthly payment. The higher the rate, the greater the payment will be. That is why it is important to know where rates are headed when deciding to start your home search.

Below is a chart created using Freddie Mac’s U.S. Economic & Housing Marketing Outlook. As you can see, interest rates are projected to increase steadily throughout 2019.

How Will This Impact Your Mortgage Payment?

Depending on the amount of the loan that you secure, a half of a percent (.5%) increase in interest rate can increase your monthly mortgage payment significantly. But don’t let the prediction that rates will increase stop you from purchasing your dream home this year!

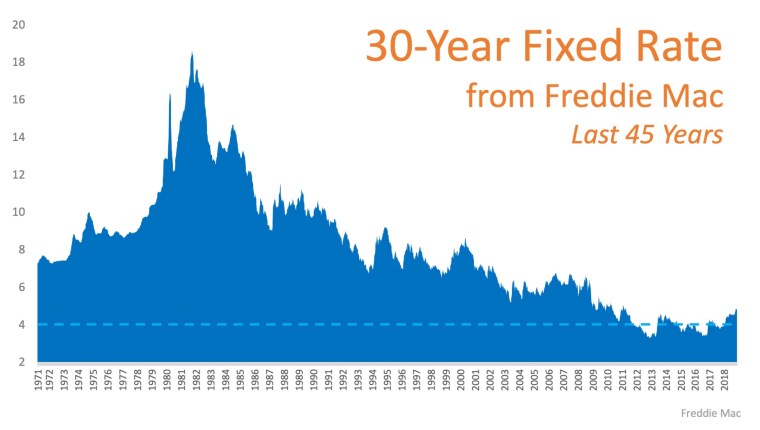

Let’s take a look at a historical view of interest rates over the last 45 years.

Bottom Line

Be thankful that you can still get a better interest rate than your older brother or sister did ten years ago, a lower rate than your parents did twenty years ago, and a better rate than your grandparents did forty years ago.

Source: keepingcurrentmatters.com

Year End Homeowner Tax Guide

One of the first steps in a good outcome is knowing a little bit about what you’re about to undertake. By being aware of some of the areas regarding homes that may not come up every year in a tax return, you’ll be able to point them out to your tax professional or seek more information from IRS.gov.

Look through this list of items for things that could affect your tax return. Even if you have relied on the same tax professional for years to look out for your best interests, they need to be aware that there could be something different in this year’s return.

If you bought a home for a principal residence last year, check your closing statement and identify any points or pre-paid interest that you or the seller paid based on the mortgage you received. These can be deducted on your Schedule A as qualified home interest if you itemize your deductions. See Home Mortgage Interest Deduction | IRS Publication 936 .

Keep track of all money you spend on your home that might be considered a capital improvement. Get in the habit of putting receipts for money spent on your home that is not the house payment or utility bills. Repairs are not tax deductible but improvements, even small ones, can be added to the basis of your home which can lower the gain when the home is sold. Years from now, your tax preparer can sift through them and determine whether they’re capital improvements or maintenance. See Increases to Basis | IRS Publication 523 Selling Your Home .

By making additional principal contributions with your mortgage payment, you’ll save interest, build equity and shorten the term of a fixed-rate mortgage. See Equity Accelerator.

If you sold a home last year, the payoff on your old mortgage included interest from the last payment you made to the date of the payoff. That interest is tax deductible. You may need a breakdown of the payoff to the mortgage company; you should be able to get that from your closing officer.

If you refinanced your home, unlike a home purchase, points paid to refinance are not deductible as interest in the year paid; they must spread ratably over the life of the mortgage. See Home Mortgage Interest Deduction | IRS Publication 936 .

For homeowners who have lost a spouse, there is an exception regarding the exclusion on the sale of a principal residence. If the surviving spouse concludes a sale of the home within two years of the death of their spouse, they may exclude up to $500,000, instead of $250,000 for single taxpayers, of gain provided ownership and use tests are met prior to death.

The two-year period begins on the date of death and ends two years after that date. See Sale of Main Home by Surviving Spouse | IRS Publication 523 Selling Your Home .

There could be significant tax consequences to a person selling a home that was received as a gift as compared to receiving the home through inheritance. With a gift, the basis of the donor becomes the basis of the donee. With inheritance, the heir usually gets a stepped-up basis and avoids potential unrecognized gain. See Home Received as Inheritance | IRS Publication 523 Selling Your Home .

This is meant for information purposes only and advice from a qualified tax professional should be sought to find out about your individual situation.

Four Reasons Not to Fear a Housing Crash in 2019 (Part 4 of 4)

There is a lot of uncertainty regarding the real estate market heading into 2019. That uncertainty has raised concerns that we may be headed toward another housing crash like the one we experienced a decade ago.

Here is the fourth of four reasons why today’s market is much different:

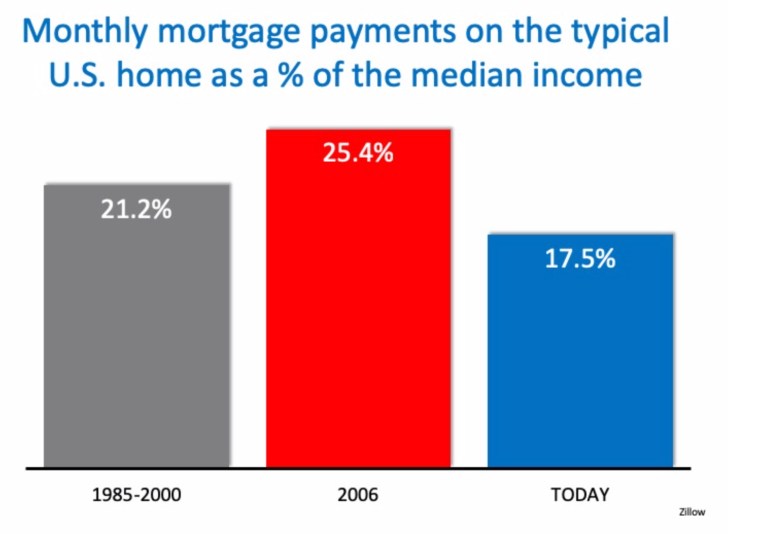

Affordability is better now than in 2006

Though it is difficult to afford a home for many Americans, data shows that it is more affordable to purchase a home now than it was from 1985 to 2000. And, it requires much less of a percentage of your income today than it did in 2006.

Bottom Line

The housing industry is facing some rough waters heading into 2019. However, the graphs above show that the market is much healthier than it was prior to the crash ten years ago.

Source: KeepingCurrentMatters.com