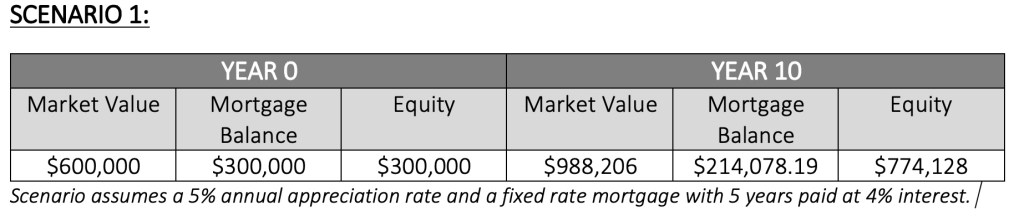

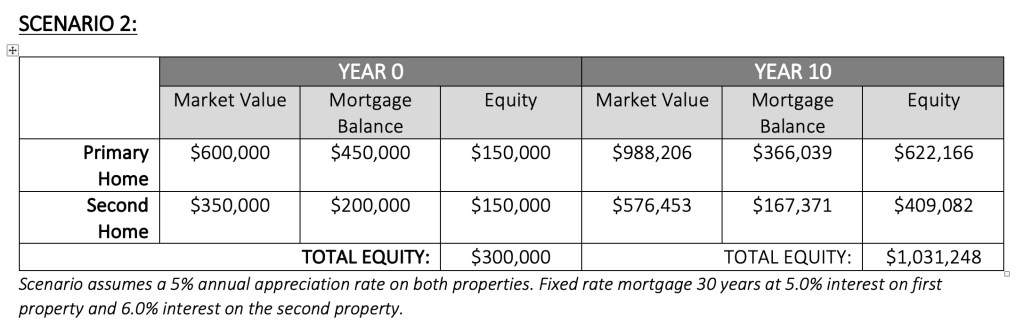

Many homeowners these days are watching their home values tick up and up and up. The difference between what you owe on your mortgage(s) and the market value of your home is known as equity. Equity minus selling expenses is what you would pocket at the end of a transaction when you sell. However, some homeowners access that equity to do other things such as home renovations or buying a second home or investment property. Buying a second home, whether it provides an income stream or not, can be a savvy way to build wealth. In the examples below, Scenario 1 shows the homeowner staying in their home for 10 years, building more equity without taking out equity or buying a second home. Scenario 2 has the homeowner taking out $150,000 in equity (in this case, we are using a cash-out refinance instead of a home equity line of credit (HELOC) though you may want to weigh both options), buying a second home, and earning equity on both homes over 10 years.

Even though the first mortgage is refinanced at a higher rate and the second home interest rate is even higher (because it is a second home), the earned equity with both homes combined is higher – $257,120 higher – than if the mortgage was simply paid down on the primary property. Why? Leverage. When the second property is purchased, the starting market value of the two properties is higher than just the single property, allowing for more room to grow.

Of course, this is just a paper example. There is no guarantee the real estate market will appreciate at 5% per year and this doesn’t take into account expenses for buying, refinancing, property taxes, maintenance, etc. It also doesn’t include income potential on the second property. Interested in learning more? Let’s talk leverage! If you are thinking about a second home out of the area, We can also connect you with a great local agent, ready to help you find a strong investment property.