The housing market has enjoyed the benefit of low mortgage interest rates for more than a decade. There has been much speculation regarding when these rates may rise. A rise in interest rates will affect buyers’ purchasing power as each increase in interest rate means less money a buyer can spend on the principal amount of a mortgage (for example, a buyer may be able to afford a $500,000 at 3% but only $470,000 at 3.25%).

How and why will interest rates change? To answer that, we need to understand the role of the Federal Reserve. The Federal Reserve, or Fed, is the central bank of the United States designed to create stability in the economy. It assesses risks such as rapid price growth, unemployment, and utilizes monetary policy to create steadiness. When the economy grows too quickly or too slowly, the Fed can make adjustments.

Since the recession of 2009, the Fed has implemented a policy to promote economic growth (achieve maximum employment and keep inflation to 2%). To accomplish this, it kept the federal fund rate close to 0% while also buying Treasury and Mortgage bonds that help control long-term interest rates (such as for mortgages).

The Consumer Price Index (CPI) increased dramatically over the last several months due to a number of factors, which has indicated an inflationary period in which prices are increasing too quickly. In fact, price increases hit a 39-year high in November 2021, with prices increasing 6.8% over November of 2020. At their December, 2021 meeting, the Fed indicated they would be changing their strategy and hence, it is expected that mortgage interest rates will be going up as a result.

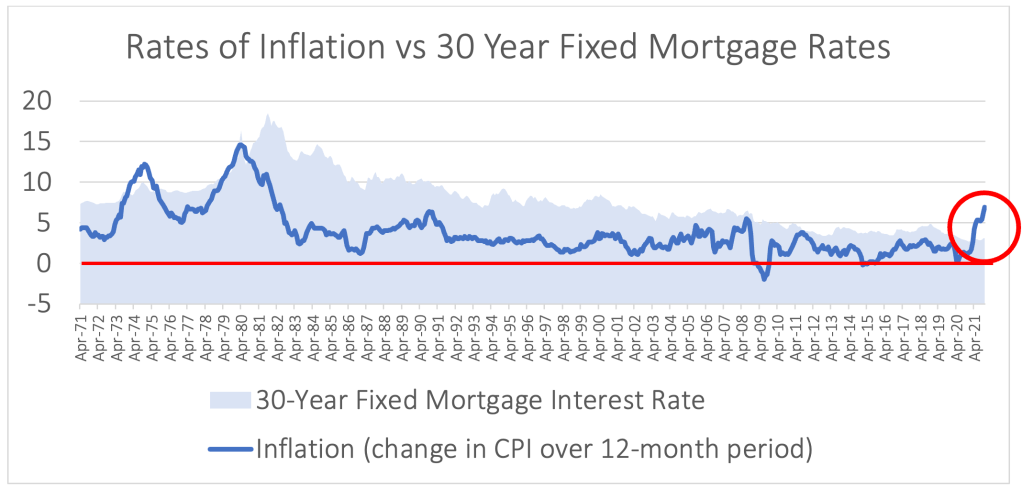

The chart above compares the rate of inflation defined as the change in the Consumer Price Index over a 12-month period (data from Bureau of Labor Statistics) against 30-year fixed mortgage rates (data from Freddie Mac) for the last 50 years. As you can see, there is a relationship between the two, and the sharp inflation we see currently is circled on the graph above and is quite evident. Historically, an inflation rate increase like we are seeing currently would have resulted in curtailing action from the Fed and mortgage interest rates would see a strong increase.

However, it is important to note that the Fed will be treading very carefully now since the economy is still recovering from COVID with new uncertainties with the variants. Furthermore, some of the price increases are due to supply chain and labor issues – not simply supply and demand. There will also be a drop in COVID-related Federal stimulus in 2022. These will all continue to impact the economy. The Fed is expected to meet again in March of 2022 and while it is expected to tread lightly when it comes to slowing the economy down, mortgage rates are expected to rise.

Sources:

Data derived from Bureau of Labor Statistics (Consumer Price Index for all Urban Consumers) and Freddie Mac’s Primary Mortgage Market Survey: Conventional, conforming 30-Year Fixed-Rate Mortgage Series.

Bureau of Labor Statistics: https://data.bls.gov/timeseries/CUSR0000SA0&output_view=pct_1mth

Freddie Mac: http://www.freddiemac.com/pmms/pmms30.html

https://www.usatoday.com/story/money/2021/12/15/fed-meeting-interest-rates/8902953002/

https://www.federalreserve.gov/newsevents/pressreleases/monetary20211215a.htm