Afraid to Sell Because You’re Not Sure You Will Find Your Replacement Home? What If We Could Buy and Then Sell

The decision to buy first or sell first, has always been a little of the “Which came first: the chicken or the egg?” type of question. Is it better to buy another home before you sell your current one or sell the current one before you buy the replacement?

Some buyers don’t have a choice because they need the equity out of the current home to purchase the new one and possibly, their income limits their ability to qualify for having both mortgages at the same time. However, some buyers, with sufficient financial resources, may have other options available to facilitate the move.

A home equity line of credit, HELOC, is a type of loan that a traditional lender like a bank will loan up to the difference in what is currently owed on the home and 75-80% of the value. A borrower is approved for the line of credit and then, can borrow against it as needed. A homeowner with sufficient equity, would want to secure a HELOC prior to contracting for the new home or listing their current one. Typically, the interest will be due monthly. When they sell the home, the loan would be paid off along with any other liens on the property like the first mortgage.

A bridge loan is different in that it is usually a specific amount of money for a short term used to “bridge” the time frame necessary to acquire the replacement property and sell the existing home. The amount available is like the HELOC, usually, up to 80% of the home’s value less the existing mortgage. Some lenders may require being in the first position which may require retiring the existing first mortgage from the proceeds from the bridge lender.

Hard money lenders are a little more flexible in some of their requirements compared to typical lenders, but it comes at a cost. They could charge two to three percent, called points, of the money borrowed and it is paid up-front. The interest rate is typically higher than long-term mortgage money.

Another alternative is to find a conventional lender who has a program that allows you to recast the loan in a specified period. The borrower would get a low-down payment mortgage on the new home and after the original home is sold and closed, the lender will apply a lump sum toward the principal amount owed on the new home and recalculate the payments and amortization schedule. By recasting the loan, the borrower does not go through the process of getting a new mortgage by refinancing and therefore saves the costs involved. Most conventional loans and conforming Fannie Mae and Freddie Mac loans allow a recast after 90-days. FHA, VA, GNMA loans do not allow recasting.

Borrowers with 401(k) retirement accounts may consider borrowing against that asset which could be a lower interest rate than other temporary options. Depending on the size of the 401(k), the amount available to borrow could be up to half the balance or $50,000 whichever is less. If the loan isn’t repaid in a timely fashion, there can be taxes and penalties.

In each of these options, the seller is involved in borrowing money to accommodate a purchase and sale of a home. There will be expenses involved but the advantage is that they have a better chance of realizing most of their equity to complete a purchase before they sell their current home. This is particularly helpful in markets that are low in inventory. It can also make moving from one house to another much easier.

One last option is to consider selling your existing home to an iBuyer or private investor. The attraction to this alternative is that they will make you an instant offer to buy your home and you’ll have cash to use to purchase your new home. These companies or investors, intend to resell the property, so they must discount the price they pay for your property taking into mind they will be responsible for repairs, maintenance, selling fees and other expenses. While it may sound appealing, you may discover that the amount you will realize will be substantially less than if you sell your home in a conventional manner.

If you have questions about Buying First and Selling Later we can do a comprehensive market analysis to indicate market value and the net proceeds you can expect to have. This will assist you in determining which option makes sense for you at this time. We can also recommend lenders and approximate timelines for each alternative.

Real Estate taxes are going up in San Juan County.

Real Estate taxes are going up in San Juan County.

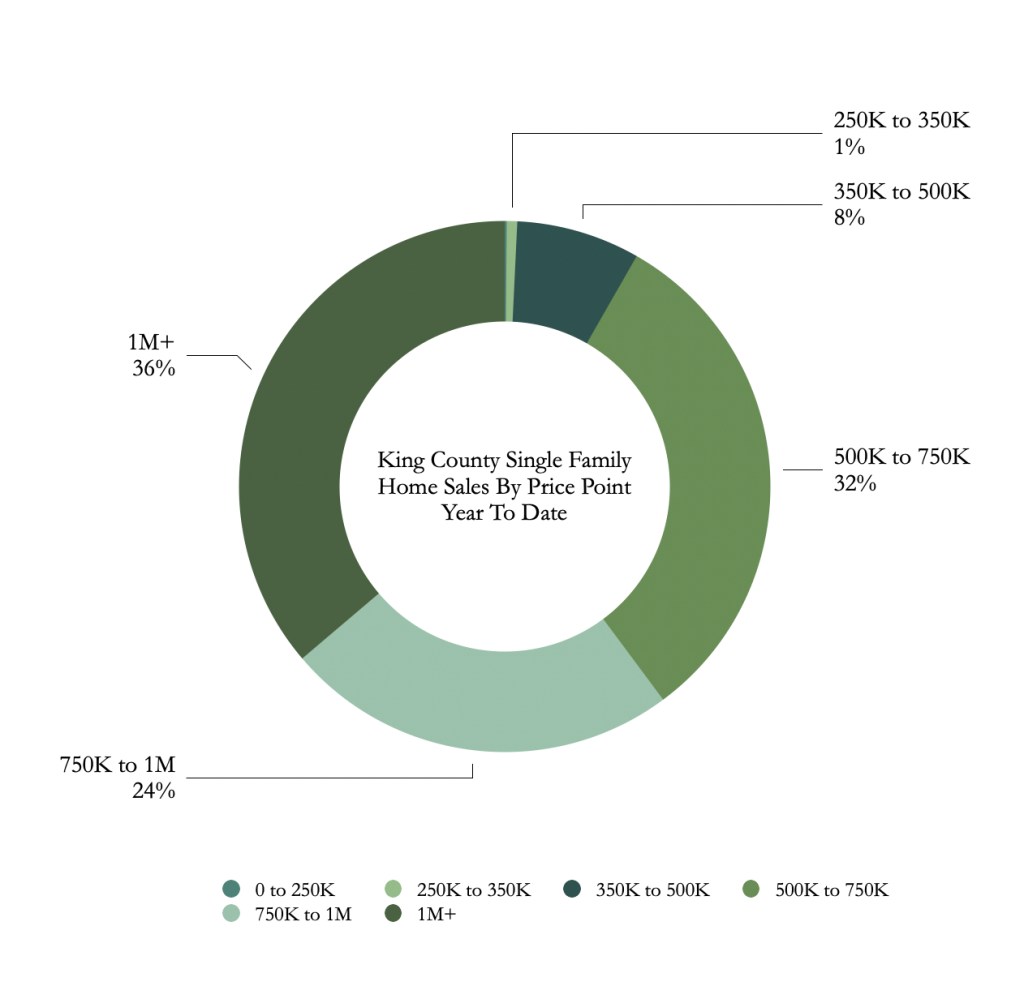

In San Juan County, where there is a 7.9 month supply of homes on the market (King County is 2.3 months) it is getting more expensive for Buyers to purchase a home.

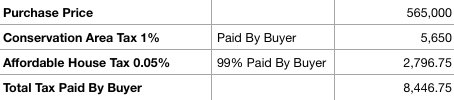

The county already imposes a Conservation Area Real Estate Tax equal to 1% of the purchase price to be paid by the Buyer at the time of closing. Now the county has added an Affordable House Excise Tax equal to 0.5% of the purchase price. The law states the new tax shall be paid 99% by the Buyer and 1% by the Seller.

In November 2018 the median selling price of a home in San Juan County was $565,000. The combined affect of these taxes raises the purchase price for a Buyer as follows:

Maybe It Is Time To Get Rid Of That HELOC

In September, the Federal Reserve raised interest rates for the third time in 2018 and they’re expected to go up one more time this year and three times next year. If you have a Home Equity Line of Credit, HELOC, you’re paying more to use that money and it is going to become more expensive.

It may make sense to refinance your home and consolidate the balance of your HELOC to lock in a lower mortgage rate. Most lenders require that the combination of these loans should not exceed 80% of the home’s fair market value and that you have good credit and adequate income to support the payment.

A HELOC is a first or second mortgage that allows the borrower to withdraw money as needed, up to the line of credit provided by the lender. A draw period is established where the borrower is only required to pay interest.

Since all HELOC loans are variable rate mortgages, during periods of rising rates, the cost of the funds increase. However, unlike adjustable rate mortgages that have specified adjustment periods and caps, a HELOC adjusts when the prime interest changes.

The formula for determining available funds on a refinance are to take 80% of the fair market value, which will probably have to be verified by appraisal, less the existing first mortgage and the costs to refinance. The balance would need to cover the cost of replacing the HELOC. Any remaining balance may be available for cash to be taken out.

Now is a great time for a mortgage review. In many cases, the equity you have in your home may allow you to eliminate mortgage insurance and substantially lower your monthly payment. As with all tax matters, always consult with a tax professional before making any decisions. Call us at (206) 979-9632 for a recommendation of a trusted mortgage professional.