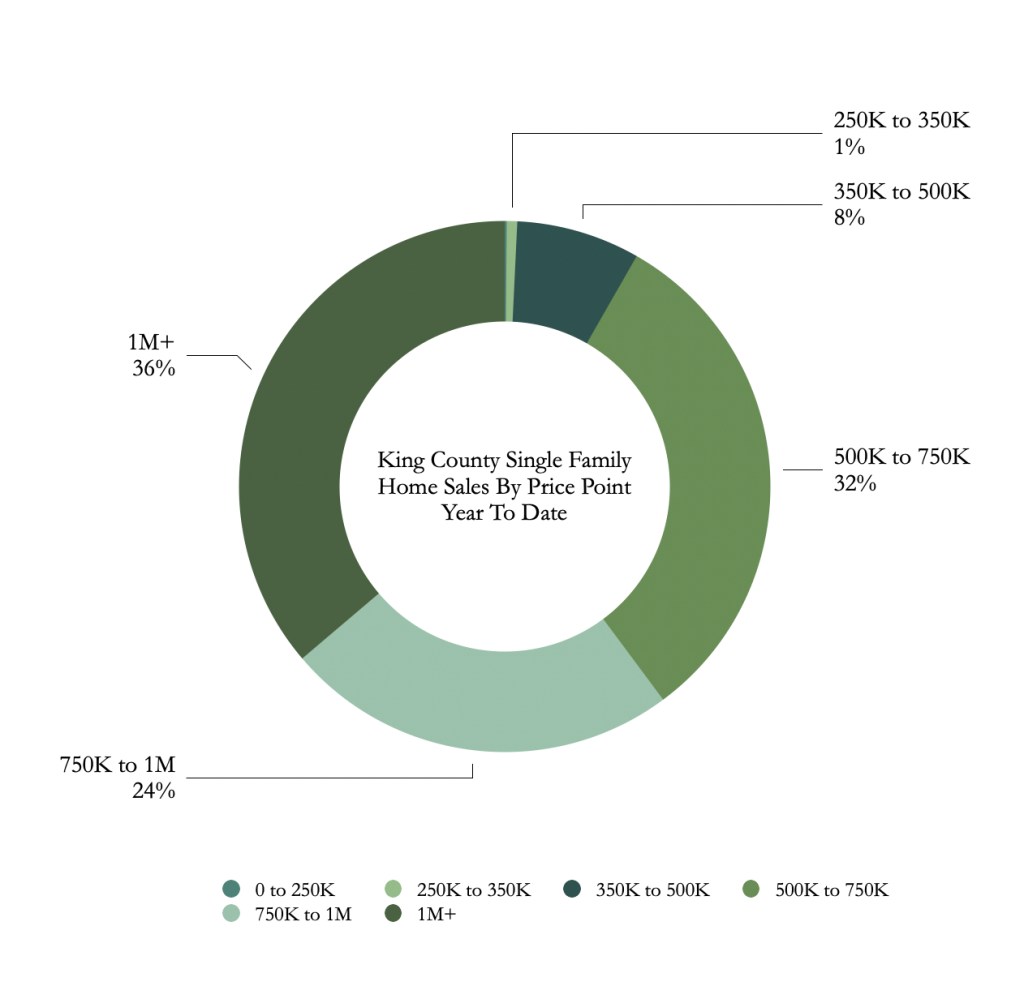

So You Like Zillow’s Zestimate?

Zillow just closed down their iBuyer program and fired 25% of their company. Their CEO says is was because they can not accurately predict home prices. We have been saying that for years.

Zillow just closed down their iBuyer program and fired 25% of their company. Their CEO says is was because they can not accurately predict home prices. We have been saying that for years.

The decision to buy first or sell first, has always been a little of the “Which came first: the chicken or the egg?” type of question. Is it better to buy another home before you sell your current one or sell the current one before you buy the replacement?

Some buyers don’t have a choice because they need the equity out of the current home to purchase the new one and possibly, their income limits their ability to qualify for having both mortgages at the same time. However, some buyers, with sufficient financial resources, may have other options available to facilitate the move.

A home equity line of credit, HELOC, is a type of loan that a traditional lender like a bank will loan up to the difference in what is currently owed on the home and 75-80% of the value. A borrower is approved for the line of credit and then, can borrow against it as needed. A homeowner with sufficient equity, would want to secure a HELOC prior to contracting for the new home or listing their current one. Typically, the interest will be due monthly. When they sell the home, the loan would be paid off along with any other liens on the property like the first mortgage.

A bridge loan is different in that it is usually a specific amount of money for a short term used to “bridge” the time frame necessary to acquire the replacement property and sell the existing home. The amount available is like the HELOC, usually, up to 80% of the home’s value less the existing mortgage. Some lenders may require being in the first position which may require retiring the existing first mortgage from the proceeds from the bridge lender.

Hard money lenders are a little more flexible in some of their requirements compared to typical lenders, but it comes at a cost. They could charge two to three percent, called points, of the money borrowed and it is paid up-front. The interest rate is typically higher than long-term mortgage money.

Another alternative is to find a conventional lender who has a program that allows you to recast the loan in a specified period. The borrower would get a low-down payment mortgage on the new home and after the original home is sold and closed, the lender will apply a lump sum toward the principal amount owed on the new home and recalculate the payments and amortization schedule. By recasting the loan, the borrower does not go through the process of getting a new mortgage by refinancing and therefore saves the costs involved. Most conventional loans and conforming Fannie Mae and Freddie Mac loans allow a recast after 90-days. FHA, VA, GNMA loans do not allow recasting.

Borrowers with 401(k) retirement accounts may consider borrowing against that asset which could be a lower interest rate than other temporary options. Depending on the size of the 401(k), the amount available to borrow could be up to half the balance or $50,000 whichever is less. If the loan isn’t repaid in a timely fashion, there can be taxes and penalties.

In each of these options, the seller is involved in borrowing money to accommodate a purchase and sale of a home. There will be expenses involved but the advantage is that they have a better chance of realizing most of their equity to complete a purchase before they sell their current home. This is particularly helpful in markets that are low in inventory. It can also make moving from one house to another much easier.

One last option is to consider selling your existing home to an iBuyer or private investor. The attraction to this alternative is that they will make you an instant offer to buy your home and you’ll have cash to use to purchase your new home. These companies or investors, intend to resell the property, so they must discount the price they pay for your property taking into mind they will be responsible for repairs, maintenance, selling fees and other expenses. While it may sound appealing, you may discover that the amount you will realize will be substantially less than if you sell your home in a conventional manner.

If you have questions about Buying First and Selling Later we can do a comprehensive market analysis to indicate market value and the net proceeds you can expect to have. This will assist you in determining which option makes sense for you at this time. We can also recommend lenders and approximate timelines for each alternative.

A successful home sale, considered by many owners, is to maximize their proceeds in the shortest time with the least inconveniences. Just because it is a seller’s market doesn’t mean that homeowners can shortcut some of the steps that make it happen and they certainly need to avoid commonly made mistakes.

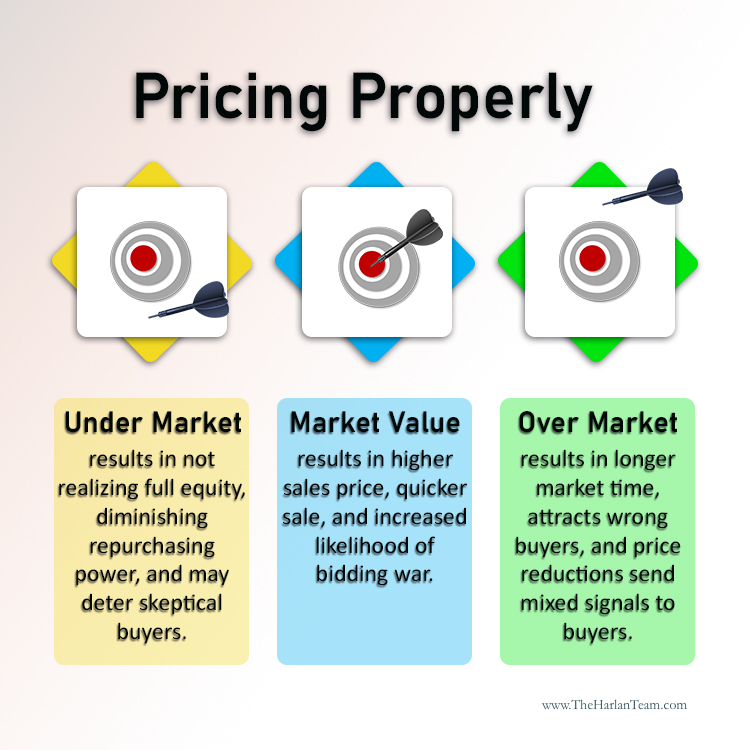

Pricing too high

Low inventory and high demand have contributed to the rising prices of homes. NAR reports that the median sales price is up 17.8% in the past year and CoreLogic recently released data that July set new record growth of 18% year over year. This might give sellers a false sense of security about overpricing their home

Pricing a home too high initially can limit activity, attract the wrong buyers and ultimately, cause the home to realize a lower price than optimum. There is an interesting dynamic that takes place when there is a shortage of homes to show, and a new home hits the market. Buyers, who have been in the market but not purchased yet, will rush out to see the home. They are familiar with what homes are selling for and possibly, have even lost bids on one or more.

These savvy buyers expect certain amenities based on the price of the home. They can tell if a home is priced right or not.

Failure to do Market Preparation

There are people who will buy a home that is not pristine and does not have everything in good working order, but they usually will not pay top dollar for the home. They recognize the money that needs to be spent and will adjust the price accordingly.

To command the highest price, the home needs to be spotlessly clean with everything working as it should be. The home needs to be depersonalized to appeal to the broadest group of people. The clutter needs to be removed so it isn’t distracting or give the impression that the rooms, counters, or closets are small.

It is important to evaluate if painting is necessary along with replacing floor covering, appliances and/or light fixtures.

Thinking the agent doesn’t matter

Market time is down to 17 days and 89% of homes are sold within a month. These statistics might be used to rationalize that an agent is not currently playing an important role in the home but that would be a mistake.

Nine out of ten homeowners use an agent, and the four most important reasons were to help sell the home within a specific timeframe, help price the home competitively, help seller market the home to potential buyers and help the seller find ways to fix up home to sell it for more money.

Being present during showings

It may not be convenient, but sellers should try to leave the home when it is being shown. Buyers like to look at the home freely and ask questions or point out things to their agent. Sellers may have the best of intentions, but they have not established rapport with the buyer and don’t really know what is causing the questions.

Not letting your agent negotiate for you

The role the agent plays as third-party negotiator is one of the most important things an agent does for a seller. It begins long before buyers even make an offer. The protocol is for the buyer’s agent to go to the listing agent with the question and if necessary, they can ask you and get back to the buyer’s agent.

Buyers and sellers have inherently different objectives. Sellers want the highest price and buyers want to pay the least. Sellers want the terms of the contract in their favor and the buyers want them to favor them. Buyers want lots of contingencies to let them out of the contract and sellers want the fewest possible contingencies. Sellers want the most earnest money and buyers want to put up the least possible.

Agents are skilled at negotiation not only because of training but also experience. Sellers’ experience is usually limited to personal transactions separated by years in frequency. Agents see multiple transactions in their daily business and can guide people through difficult areas.

Not responding to offers in a timely manner

Normally, an offer can be withdrawn, at any time, up until the point that it is accepted. The expression a bird in the hand is worth two in the bush reminds us that the offer you have is real and the ones in the bush, may never come to fruition.

A common situation occurs when there is large amount of activity on the home and an offer comes in quickly. Instead of negotiating on that offer, the sellers wait to see if any better ones are received. By waiting, the seller runs the risk of the buyer changing their mind.

Alternatively, in the same situation described, the seller may decide to put the home on the market on Saturday morning and let prospective buyers know that they will be deciding on all offers received over the weekend on Sunday evening.

Your agent is a valuable part of selling a home who can offer advice, bring perspective to the transaction, and suggest different ways to help you achieve your goals. Once you have the right agent, everything else will start to fall into place.