Maybe It Is Time To Get Rid Of That HELOC

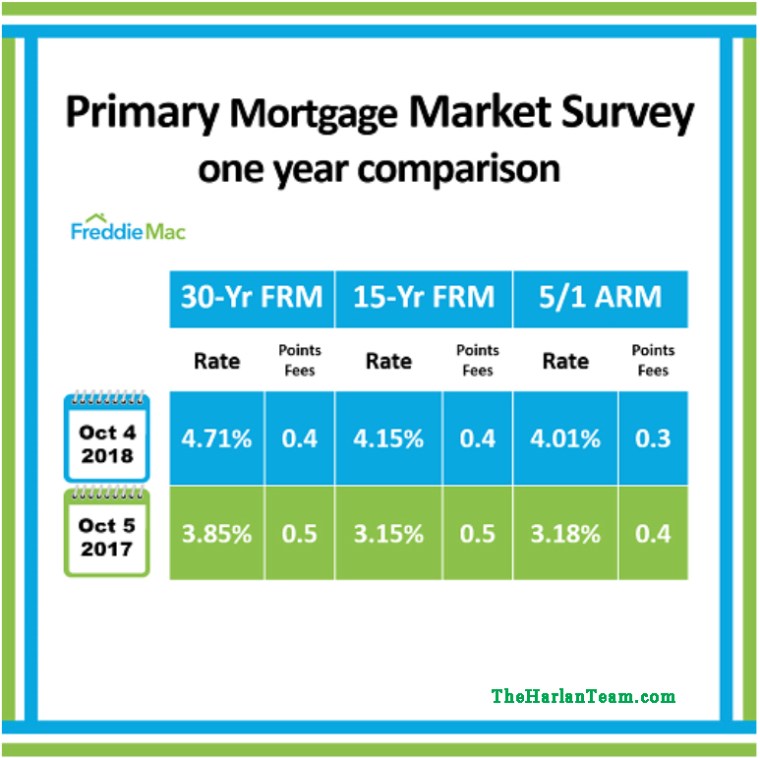

In September, the Federal Reserve raised interest rates for the third time in 2018 and they’re expected to go up one more time this year and three times next year. If you have a Home Equity Line of Credit, HELOC, you’re paying more to use that money and it is going to become more expensive.

It may make sense to refinance your home and consolidate the balance of your HELOC to lock in a lower mortgage rate. Most lenders require that the combination of these loans should not exceed 80% of the home’s fair market value and that you have good credit and adequate income to support the payment.

A HELOC is a first or second mortgage that allows the borrower to withdraw money as needed, up to the line of credit provided by the lender. A draw period is established where the borrower is only required to pay interest.

Since all HELOC loans are variable rate mortgages, during periods of rising rates, the cost of the funds increase. However, unlike adjustable rate mortgages that have specified adjustment periods and caps, a HELOC adjusts when the prime interest changes.

The formula for determining available funds on a refinance are to take 80% of the fair market value, which will probably have to be verified by appraisal, less the existing first mortgage and the costs to refinance. The balance would need to cover the cost of replacing the HELOC. Any remaining balance may be available for cash to be taken out.

Now is a great time for a mortgage review. In many cases, the equity you have in your home may allow you to eliminate mortgage insurance and substantially lower your monthly payment. As with all tax matters, always consult with a tax professional before making any decisions. Call us at (206) 979-9632 for a recommendation of a trusted mortgage professional.

–

–